If you’re like me, from time to time, you wonder where your KiwiSaver money is invested.

Your KiwiSaver is made up of income and growth assets or a varied mix of the two types. Income assets are generally debt funding like cash, bonds, and fixed-term deposits. Income assets are paid interest and there is a high expectation of the investor getting their money back. Due to this expectation of money back after a fixed term, they’re seen as less risky and offer lower returns. On the other hand, growth assets usually generate capital growth as well as dividends. Growth assets are typically shares in companies (equities), infrastructure, and property investments. These growth assets carry higher risk with the acknowledgment that the investor can lose money or underperform expectations. As a result, they offer higher potential returns.

Most KiwiSaver providers have a similar investment structure to one another. They offer different funds made up of different types of assets that vary in volatility, risk, and return. More specifically, these investments can be broken into cash and fixed interest, which are regarded as income assets. On the other hand, NZ property, Trans-Tasman Shares, and International Shares are regarded as growth assets. Typically, the difference in performance comes from the specific companies and assets they invest in at any particular time.

However, performance isn’t the only criteria or reason for choosing to invest in one KiwiSaver provider over another. We as consumers have become increasingly aware of environmental and ethical issues that businesses can get involved in. Many people care and will make a proactive decision to look for more ethical alternatives. This is where the point of ethical investment comes in. What exactly do we mean by it and what are providers doing to improve their standards of investment.

Cash – Income Assets

Generally, cash assets are regarded as the most stable of investments, offering low risk and lower returns. Many Cash and Conservative funds hold higher percentages of cash assets as part of their portfolio.

Cash assets themselves are fairly self-explanatory. It is holding your investment in cash or the equivalent of cash. This makes the investment liquid, meaning easy to withdraw (if applicable), and less exposed to the volatility of external factors. Holding your savings in a bank account is also considered a cash asset.

According to the Milford KiwiSaver Cash Fund, this is a low-risk asset for people needing to withdraw their money in the short term. Particularly when people want to use their investment to purchase a first home soon. Many providers offer Cash Funds made up of 100% income assets. These assets are defined primarily as New Zealand cash, short-dated debt securities, and term deposits. The objective of most Cash Funds is to target an investment return higher than the NZ Official Cash Rate.

Aside from specific Cash Funds made up entirely of cash and equivalent assets, other fund types can hold cash too. Here’s an example of 4 KiwiSaver providers and their cash assets in 3 of the fund types they offer:

Cash & Cash Equivalents Allocation as a Percentage of Total Fund (December 2021)

| Fund: |

ANZ |

Generate |

Milford |

Simplicity |

| Conservative |

27.64% |

3.66% |

16.76% |

2.60% |

| Balanced |

16.01% |

– |

20.87% |

3.59% |

| Growth |

6.06% |

4.40% |

16.21% |

3.12% |

During turbulent times, some providers may decide to hold higher than targeted cash assets in order to minimise volatility. In addition, holding cash allows investors to pounce on great opportunities should they arise as the market recovers.

Fixed Interest – Income Assets

A fixed interest asset can be thought of as a loan to reliable entities such as governments or large corporations. They can be local New Zealand assets or international. Fixed interest assets are considered as slightly higher risk than cash but lower risk than growth assets, such as shares.

Fixed interest assets can include things like government bonds and corporate bonds. They are essentially a loan at a fixed interest rate and set intervals, and normally a specific payback period. There is a high expectation that the principal amount is going to be repaid at the end of the term.

As a result of the slightly higher risk, fixed interest returns tend to be slightly higher than cash asset returns. However, they generally offer lower returns than shares and property assets.

Funds that are heavily invested in fixed interest assets strive for certainty and reliability as their investment strategy. In addition, fixed interest assets have a role to play even in riskier funds as part of a diversification strategy.

Here’s an example of fixed interest investment across 3 different funds offered by 4 different providers:

Fixed Interest Allocation as a Percentage of Total Fund (December 2021)

| Fund: |

ANZ |

Generate |

Milford |

Simplicity |

| Conservative |

48.52% |

62.53% |

68.64% |

75.15% |

| Balanced |

30.14% |

– |

29.56% |

40.68% |

| Growth |

9.18% |

13.20% |

14.79% |

19.45% |

NZ & International Property – Growth Assets

Property refers to investments in real estate. Funds can invest in property trusts or real estate development companies. Properties are growth assets and they can be publicly listed or come under an unlisted category. Normally, property assets can generate earnings through capital gains and developing or leasing. When seeking capital growth, property investments should be seen as a longer than 5-year investment. On the other hand, if your goal is generating stable income through leasing, your investment window can be between 1 to 2 years.

Property is seen as a medium-risk investment in between cash and fixed interest (lower risk) and shares (higher risk). Accordingly, it is also an asset offering potentially medium returns over a longer-term.

While the Simplicity KiwiSaver Scheme doesn’t hold any property assets as shown in the table below, other providers do. Property assets are used as part of the KiwiSaver mix to diversify the investment portfolios. There is no definitive right or wrong answer as to how much property your provider should be invested in.

Property Asset Allocation as a Percentage of Total Fund (December 2021)

| Fund: |

ANZ |

Generate |

Milford |

Simplicity |

| Conservative |

2.78% |

6.09% |

3.60% |

0.00% |

| Balanced |

6.87% |

– |

7.00% |

0.00% |

| Growth |

9.99% |

12.30% |

5.18% |

0.00% |

Trans-Tasman Shares – Growth Assets

Trans-Tasman shares are investments into New Zealand and Australian companies listed on each country’s stock exchange. These shares are regarded as growth assets.

Although international assets play a bigger role in funds seeking higher returns, providers also invest in local companies. Simply on a size factor, investing in international companies can offer large benefits and potentially much higher returns. However, one can argue that investing in local companies is a great way to strengthen the local Trans-Tasman market. The majority of KiwiSaver funds invest significantly in Trans-Tasman assets.

Here’s an example of four providers and the percentage of Trans-Tasman shares as part of their investment mix:

Trans-Tasman Shares Allocation as a Percentage of Total Fund (December 2021)

| Fund: |

ANZ |

Generate |

Milford |

Simplicity |

Conservative |

3.35% |

11.05% |

4.93% |

9.52% |

Balanced |

9.42% |

– |

20.56% |

20.74% |

Growth |

14.77% |

22.33% |

29.15% |

29.13% |

The majority of this portion is invested in publicly listed companies on the NZ and Australian stock exchanges. However, they can also be invested in privately-held local companies. What particular local businesses does my provider invest in? That is something you can find more about by logging into your KiwiSaver login and inspecting your fund fact sheet.

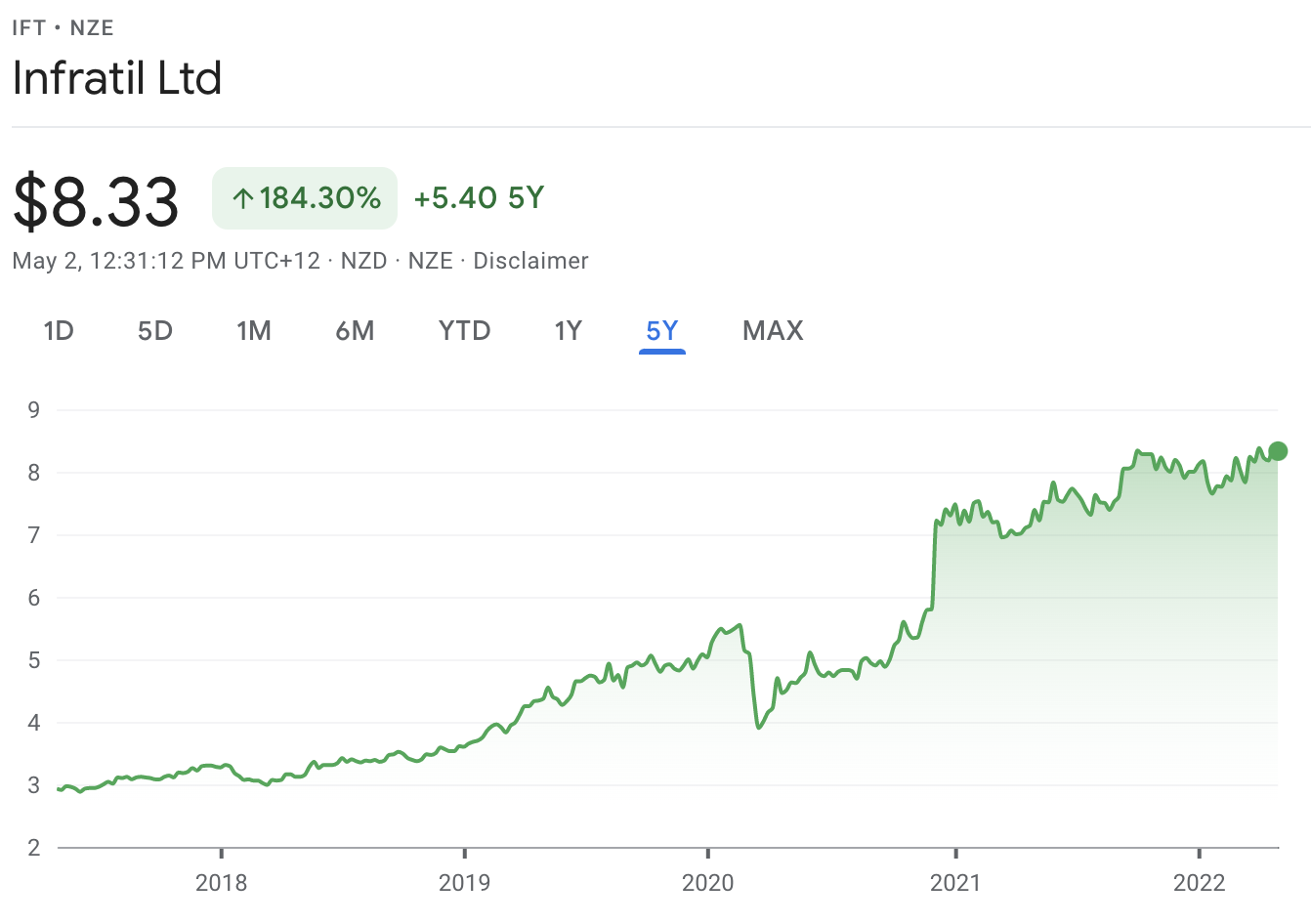

For example, Generate has invested 6.14% of its Growth Fund holdings into Infratil, a New Zealand company. Infratil is an infrastructure investment company with assets in renewable energy, airports, healthcare, and digital infrastructure sectors.

The company’s share price has grown 184.30% in the last 5 years (as of May 2nd, 2022). The Generate growth fund is directly impacted by its asset holdings such as Infratil and each asset’s performance.

Fund managers in different KiwiSaver Schemes choose which local companies to invest in on behalf of their shareholders.

International Shares – Growth Assets

International shares are investments into companies listed in global markets such as the USA, Europe, India, and China. International shares are also regarded as growth assets.

By accessing KiwiSaver login you can go into your fund details and find a breakdown of the biggest asset holdings. Here’s a breakdown of some funds offered by ANZ, Generate, Milford, and Simplicity, and their makeup of international assets. Generally, the higher risk funds with higher historical returns are more invested in international shares because of the greater opportunity.

International Shares Allocation as a Percentage of Total Fund (December 2021)

| Fund: |

ANZ |

Generate |

Milford |

Simplicity |

| Conservative |

16.43% |

16.67% |

5.87% |

12.73% |

| Balanced |

35.21% |

– |

21.86% |

35% |

| Growth |

56.50% |

47.77% |

34.19% |

48.30% |

As an example, we can also compare the difference of the biggest international asset holdings between the four providers. Based on the international asset mix and performance at any point in time, some will provide higher results than others.

Comparison of Biggest International Asset Holdings as a Percentage of Total Growth Fund (December 2021)

|

ANZ |

Generate |

Milford |

Simplicity |

||||

|

Asset |

Country |

Asset |

Country |

Asset |

Country |

Asset |

Country |

|

Visa Inc (1.34%) |

USA |

T Rowe Price Global Equity Fund (6.69%) |

Australia |

Virgin Money UK PLC (2.68%) |

UK |

Vanguard Ethically Conscious Int Shares NZD (31.43%) |

Australia |

|

Nestle SA (1.07%) |

Switzerland |

Magellan Global Fund (3.91%) |

Australia |

Alphabet (2.05%) |

USA |

Vanguard Ethically Conscious Int Shares AUD (16.88%) |

Australia |

|

Thermo Fisher Scientific Inc (0.87%) |

USA |

Berkshire Hathaway (3.73%) |

USA |

Microsoft Corporation (1.96%) |

USA |

– |

– |

|

Schneider Electric (0.80%) |

France |

Worldwide Healthcare Trust (3.11%) |

UK |

HCA Holdings Inc (1.87%) |

USA |

– |

– |

|

Accenture Plc – Class A (0.76%) |

USA |

Alphabet (2.49%) |

USA |

CRH Plc (1.81%) |

Ireland |

– |

– |

Ethical Investment Initiative

Ethical investing is a broad and difficult subject to navigate through. Partly because different viewpoints can make it a minefield of a discussion to have. There are some ethical topics that the majority can agree on and others that divide opinion.

As of December 2021, MBIE announced a couple of changes to default fund criteria that relate to ethical investing. Investment in fossil fuels and illegal weapons is prohibited in default funds. In addition, default providers have to include a responsible investment policy on their websites. This essentially means they have to elaborate on their investment strategy and their position on environmental, social, and governance factors. Many of the remaining providers have followed suit and applied some or all of the government-inspired ethical investing criteria.

On the other hand, you have some topics that divide opinion. In 2021 the Facebook Files by the Wall Street Journal made headlines about the platform’s ethically questionable user-focused decisions. Time and time again Amazon.com has been the subject of scrutiny due to low staff wages and safety concerns. The Guardian wrote an article on how Nike was forced to make some ethical improvements after strong activism.

As consumer intent toward ethical choices grows, many companies have been forced to adapt or lose customers. The same goes for all KiwiSaver providers. Many people may consider transferring KiwiSaver to another provider for ethical reasons rather than for higher returns.

Conclusion

Like myself, you may be wondering how your investment is being managed and where exactly the money goes. Finding out more is relatively easy to do so through your KiwiSaver login or your provider’s website. By selecting your chosen fund, you can find out the top 10 investments that make up the particular fund. Each fund also has a detailed breakdown of the investment mix by asset type.

Assets come into two categories, income, and growth. Income assets are things such as cash and fixed interest holdings. They are typically lower risk while offering lower returns. In addition, the higher risk funds include significant portions of growth assets like property, Trans-Tasman, and international shares. These growth assets have a history of higher growth in the long term but are exposed to short-term fluctuations.

Moreover, there are many Kiwis who value ethical investing over the best performing KiwiSaver funds. Most providers have taken steps to minimise or eliminate their exposure to investments in fossil fuels and illegal weapons. However, there are other ethical topics of debate that are more difficult to navigate. Companies like Amazon, Nike, and Facebook, have all been scrutinised in the past for things like workers’ compensation and overreach. These companies continue to be part of the investment mix of many providers and it can be difficult to draw a line. However, many providers are increasingly aware that their impact on environmental, social, and governmental issues can sway consumer choice. Thus, it is in their best interest to create an ethical investment policy along with striving to deliver high returns.