KiwiSaver managers are currently not required to provide or offer financial advice for their customers like yourself. Of the 30+ KiwiSaver providers, there is a wide variety of levels of advice offered; from no advice at all right through to personalised advice from independent financial advisers.

We’ll investigate what that means for you and whether providers should be required to give their members access to personalised financial advice.

But before that, let’s explore if receiving financial advice is actually worth it or not?

How could financial advice help me?

The idea that financial advice has a positive impact on personal finances is not a new one. The Financial services council gathers data, and has recently released a study on the impacts of a financial advisor. They found that New Zealanders are in worse financial shape than they think, and many would be unable to sustain their lifestyle for more than a month if they lost their job.

They also released statistics on the type of people who generally seek financial advice. High earners are much more likely to seek financial help and their KiwiSaver balances are on average 50% higher than people who do not seek financial advice. This is widening the gap between high and low-income earners, and further disadvantages low-income earners.

Low-income earners are already on the back foot, without the support of financial advice they are receiving an average of 4% less on their KiwiSaver investments and save 3.7% less of their income. The gap is widening more and more which is why it is so important for everyone to have access to financial advice.

Not only have they found financial benefits to receiving financial advice, they also found that financially advised members have a much higher level of satisfaction. In fact, out of six satisfactory indicators, financially advised individuals were happier in all categories:

| Are you happy with your KiwiSaver provider on the following? | % of satisfaction of Advised members | % of satisfaction of Not advised members |

| Trustworthiness |

69.6% |

54.3% |

| Member communications |

71.2% |

50.1% |

| Member service/support |

72.1% |

49.4% |

| Competitiveness of investment performance |

68.8% |

47.9% |

| Competitiveness of fees |

54.2% |

40.5% |

| Fairness of fees |

57.0% |

38.7% |

(Source: Financial Services Council: Money & You)

Last year when the market hit a road bump with Covid, over 256,000 Kiwi’s changed funds, primarily from growth to a conservative or cash fund. This locked in the loss made by the growth fund and the result was that New Zealanders lost over $820 million in their KiwiSaver accounts alone! If everyone had financial advice before being able to make that decision, a financial advisor could have explained that market dips are part of investing, and returns have since recovered in almost all areas.

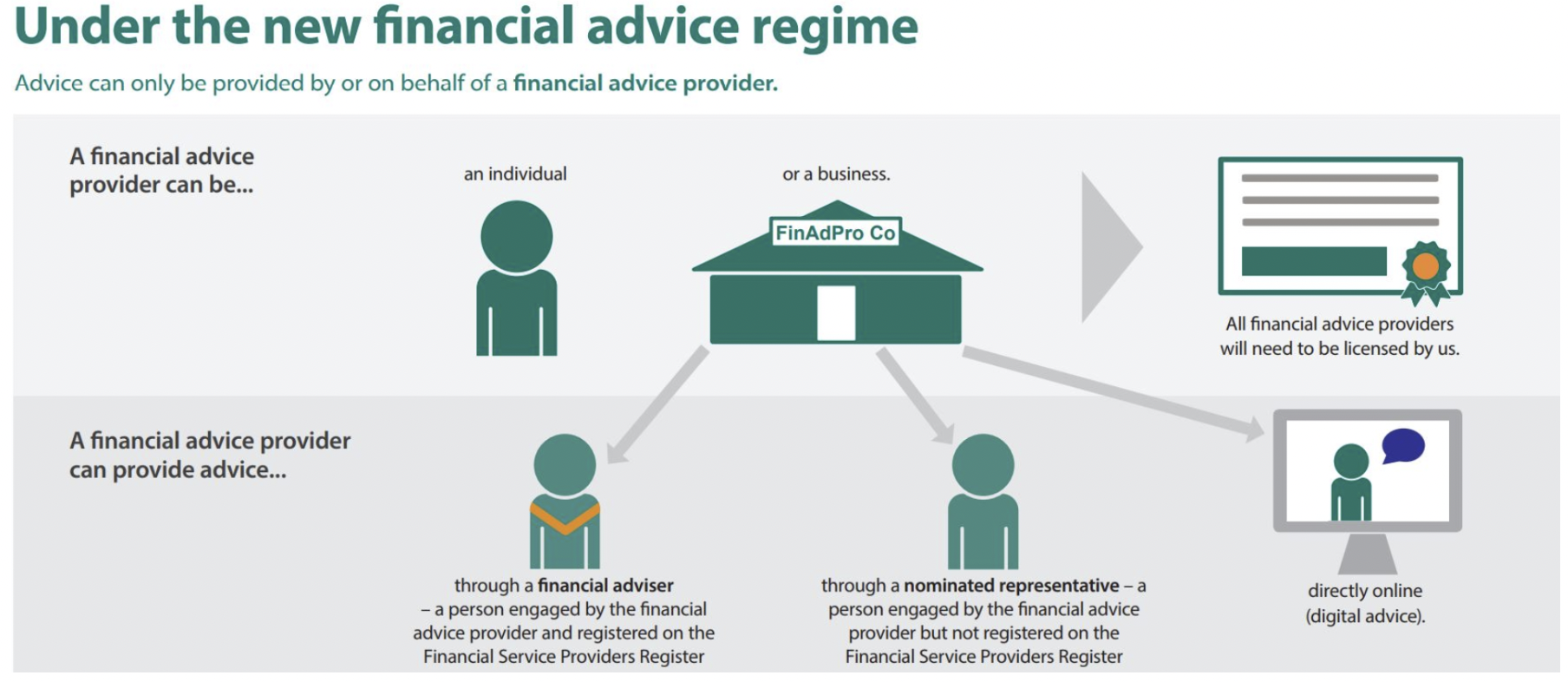

Financial advice NZ: Can anyone give it?

Personalised financial advice is a financial service in which the client receives advice on their finances relative to their personal situation. To give financial advice in New Zealand, one must be registered with a financial advice provider (FAP). Providers who provide financial advice will be FAP’s. Not all KiwiSaver providers offer financial advice, however. All providers are registered under the Financial Services Providers Register, and those providers who offer financial advice will also be FAP’s.

(Source: FMA)

Which KiwiSaver providers don’t offer advice? Why?

There are a number of providers who choose not to provide and offer financial advice. In general, the lower cost providers will be the ones who do not offer personalised advice. They choose instead, to pass the low costs onto their customers, which for some is well worth it.

Let’s take a closer look at some of the providers who do not provide financial advice.

Simplicity

Simplicity is a provider that is well known for its simple, low fee structure, and ethical values. They have been announced as one of the new default providers when the new structure changes on December 1, 2021.

Simplicity is able to save money by not employing financial advisors, and pass these savings onto their customers. The average Simplicity customer will pay $82 in fees per year, whereas the average member will pay $210.70 (based on a $20,000 KiwiSaver balance, information gathered from the Morningstar 30 June 2021 report).

Simplicity’s business model is great if you are financially savvy. If you are looking for a provider at a low cost and doing good for the community, they could be one of your choices. Unfortunately, most of us aren’t that financially savvy and don’t understand the in’s and out’s of investing. That is where the value of financial advice can really thrive.

Juno

Juno is another provider who does not offer financial advice. Juno has a unique fee structure, where they only charge a set fee on your balance instead of a fee based on the percentage of your fund. This alternative structure is designed to be more transparent for customers, instead of being charged a percentage of your balance each month, Juno customers know that they will always be charged $8 every month, year on year.

Although Juno is not one of the chosen default providers, they have some of the lowest fees in the country, with their average annual fee costing $96 per year (based on a $20,000 balance in any fund).

We can start to see a pattern here. Providers who focus primarily on low fees seem to avoid any added internal costs such as employing financial advisors or paying for clients to seek independent financial advice. As we said above, these types of providers are great for financially savvy kiwi’s who are wanting the most ‘bang for their buck’. In saying this, we know that not everyone fits the same mould, and we do not recommend this for anyone who does not understand the intricacies of investing.

Which KiwiSaver providers offer independent advice? What’s the catch?

Some providers offer independent financial advice, which is where the financial advisors don’t work directly for the provider. In general, providers who offer this access to independent advice have higher costs than those who do not offer advice. But as we have also seen above, the value that a financial advisor can add is huge, and a lot of people feel that the added cost is worth the advice given.

Let’s take a closer look at some providers who offer independent financial advice.

Fisher Funds

Fisher Funds is a provider that consistently makes headlines with excellent returns in their actively managed KiwiSaver funds. They have a rigorous company acceptance regime to ensure they only invest with companies aligned to their ethical principles. They are proving to be one of the top competitors in terms of fund performance.

Fisher Funds also pay for all their clients to receive financial advice – for free! They see the individual value in each client and want to maximise success in everyone’s KiwiSaver accounts.

Fisher Funds are one of the providers who pretty much offer everything. Due to all of the added services such as actively managed funds, personalised financial advice, quarterly updated investment choices through their own ethical select committee, their fees are higher than some others, with an average annual cost of $218 (based on a $20,000 balance in a balanced fund). But even after the higher fees, their returns have been consistently among the top performers compared to other providers, so for many, the higher fee is well worth it.

Booster

Booster is another default KiwiSaver fund. Unlike Simplicity, Booster has been a default fund in the past and has been chosen as one of four providers to retain the default status. Also unlike Simplicity, Booster is an example of a default provider who does offer financial advice. Booster says they have over 400 advisors across New Zealand to help set your path in the right direction. David Copson of Booster says “Over a lifetime, the value a financial advisor adds to your investment is the difference between a ‘good’ or ‘great’ retirement”.

Booster offers a one-off in house financial advisory service and also provides access to independent financial advisors for all of their KiwiSaver members – for free! Similarly to Fisher Funds, the added costs of working with financial advisors is reflected in their fees, with an average annual cost of $258 (based on a $20,000 balance in a balanced/moderate fund).

Milford Assets

As well as offering access to independent financial advisers like Booster and Fisher, Milford Assets also offer a simplified version of financial advice, where customers can receive financial advice online. It is not as comprehensive a service as a financial advisor would give, but it is nice to see a company offering more than one type of advisory service for their customers.

Milford’s digital advice only provides advice on Milford related products and does not offer wider services for advice on your personal finances outside of KiwiSaver investing. As with other funds, this is included in the regular fund fees and therefore essentially no extra cost to you. The average annual fee you can expect to pay with Milford is $212 (based on a $20,000 balance in a balanced fund).

Please take note that the above lists are not comprehensive and do not include all KiwiSaver providers.

Are there KiwiSaver providers in the ‘middle’?

To a certain extent, yes. Many providers have detailed information about investing on their websites and offer ‘in house’ financial advice. BNZ is an example of this. They won the Canstar Outstanding Value KiwiSaver scheme Provider award for their low fees and excellent customer service and offerings.

BNZ actively encourages members of their default fund to make an informed decision of where they should invest. BNZ doesn’t offer independent financial advice as Fisher Funds do, instead, they have chosen to structure their funds in a simple format with as much information as possible available on their website for customers to make their own decision. They also offer ‘in house’ financial advice, which is a step in the right direction of helping Kiwi’s become financially literate.

The biggest issue with this approach to financial advice is that not everyone learns the same way. Hands up if you would ever, or have ever, taken the time to read the information on your providers’ website. Who here knows details about the companies that your KiwiSaver fund is invested in? Who has ever had the intention of reading the information but got confused or overwhelmed and gave up?

For some, these aren’t issues and you won’t need financial advice which is great! But for others, this is a very real struggle and that is ok too. This is why having financial advisors help someone with their personal financial situation is important. The level of value that a financial advisor can offer is so much more than what’s written on paper and a lot of Kiwi’s need this added level of advice to fully understand their KiwiSaver investment choices.

If KiwiSaver Providers provide advice, why do I need a company like National Capital?

The difference between getting advice from National Capital versus a provider is that a provider will only advise on their own KiwiSaver funds. National Capital on the other hand is an independent financial adviser and will advise you on which of the multiple providers and over 200 funds on its research list is the best fit and value for money for you. This service is also provided at no cost to you. We are paid directly by the providers, so a win-win!

National Capital only focuses on giving advice. We don’t manage money as the providers need to, and that means that our concentration is solely on the quality advice that we can offer our clients.

Although it would be nice, not everyone knows about independent financial advice companies such as National Capital. We value the importance of the providers themselves having the tools to give anyone who could need it, the advice to help them find the best fund for them.

Having access to financial advice is crucial in levelling the playing field for all Kiwis in terms of their success with their funds. If you’re unsure about your fund, ask your KiwiSaver provider. They are there to help. If you want to check that you are in the right fund or with the right provider for your situation, feel free to complete National Capital’s free KiwiSaver Healthcheck and we will recommend a fund that suits your needs.