The COVID-19 pandemic has caused an unprecedented human and health crisis. Measures have been taken across the globe to fight and contain the spread of the virus which has triggered a major economic downturn. Global markets have fallen like dominoes in a matter of days and countries around the world are suffering due to the destabilised economy. The length and severity of the pandemic’s impact are unknown which throws the future into a whirlwind of uncertainty.

In this article, we aim to update our clients by covering how Milford Asset Management is managing its Active Growth Fund during the COVID-19 pandemic. Overall, Milford claims they are cautiously positioned with their client’s investments and taking advantage of carefully selected opportunities as they present themselves. Milford believes the financial markets have experienced a partial rebound in the month of April as the world continues to digest the fall out of the COVID-19 pandemic.

We will look at some of the commonly asked questions and their responses from the portfolio manager and deputy CIO Jonathan Windust. Furthermore, this article will explore some of the tactical decisions and opportunities Jonathan Windust has taken by looking at the analytical data used to make these complex decisions.

What has Milford done to help cushion the Active Growth Fund against falls in the share market?

Firstly, Milford reduced their allocation in shares. Shares are highly volatile assets and their prices have been severely impacted by COVID-19.

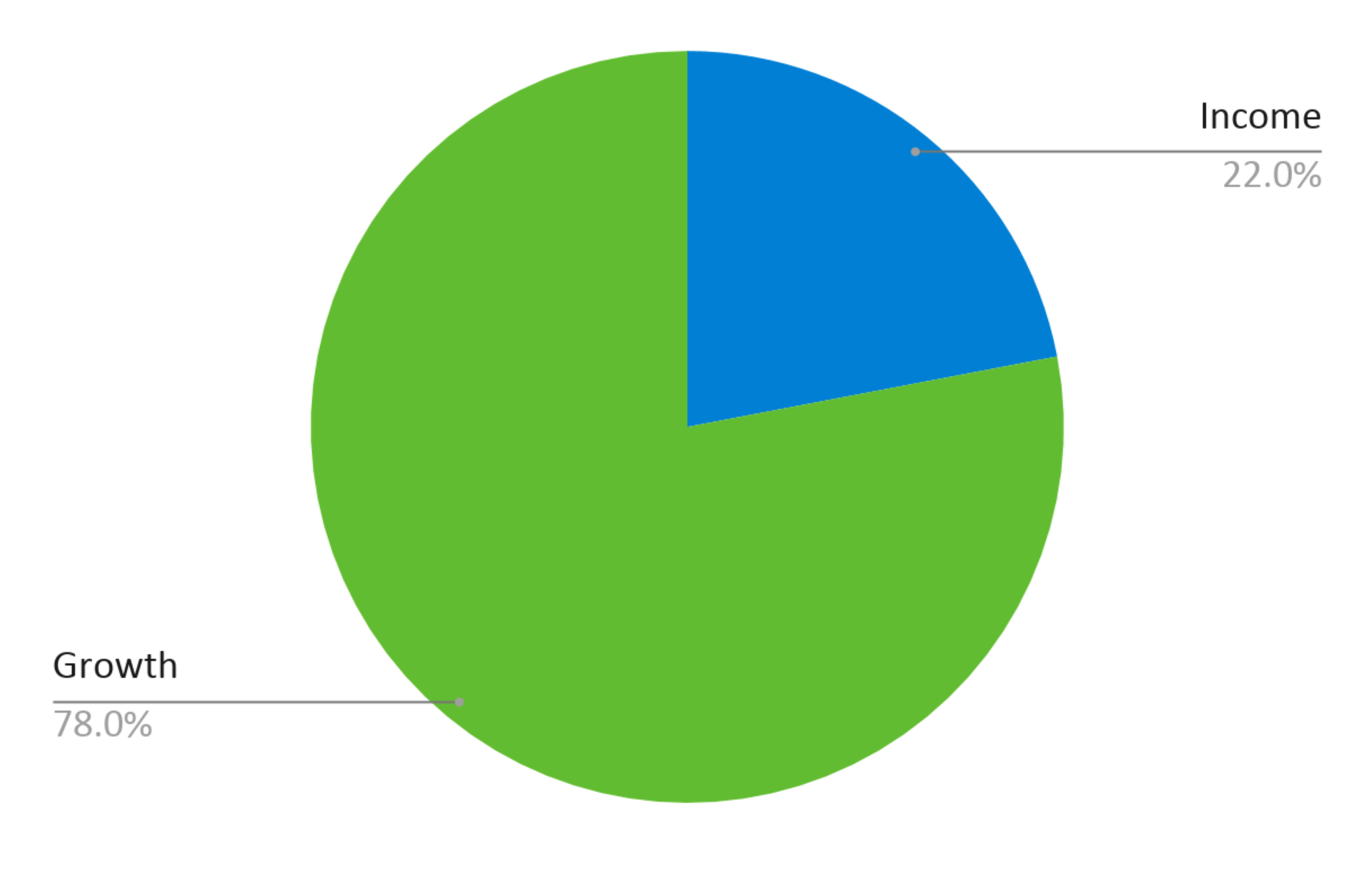

Growth funds are focused on long term growth. They tend to invest largely in growth assets which yield a higher return than other asset classes (such as income assets) but have a higher risk. Milford’s Active Growth Fund typically has approximately 80% invested in shares. According to the quarter fund update of December 2019, the Active Growth fund had 78% invested in growth assets such as commodities, global shares, alternative assets, trans-Tasman shares, and real assets.

When Milford became concerned about the coronavirus, and it spread out of China and across the globe, they reduced the allocation to shares in the Active Growth Fund to below 60%.

Milford empowers its Portfolio Managers of individual Funds with the autonomy to make tactical asset allocation decisions within the defined allocation ranges for each Fund. Portfolio Managers make these investment decisions on an active and continuous basis to improve the risk-adjusted returns of the Funds.

Below is a table that explains the level of deviation the manager has when determining the weights for this fund:

| Asset Class | Benchmark Asset Allocation (long-term bench mark) | Minimum | Maximum |

| Cash | 6.00% | 0.00% | 70.00% |

| NZ Fixed Interest | 4.00% | 0.00% | 70.00% |

| International Fixed Interest | 12.00% | -10.00% | 50.00% |

| Australasian Equities | 46.00% | 10.00% | 100.00% |

| International Equities | 32.00% | 0.00% | 60.00% |

| Growth Investments | 78.00% | 20.00% | 100.00% |

| Income Investments | 22.00% | 0.00% | 80.00% |

(Source: Milford Asset Management)

*A negative minimum value indicates that Milford is able to use short selling, or the use of derivatives to achieve the fund objectives. While borrowing is not allowed, they might invest in funds that do.

Secondly, Milford changed the type of shares the Active Growth Fund invested in. Milford declares they are avoiding shares that they believe are going to be directly impacted by the coronavirus such as the tourism and travel sectors. They are also avoiding investing in shares in highly leveraged companies. Leverage (or gearing) is borrowing money to increase return. A high operating leverage indicates a company has a large proportion of fixed costs, meaning the company is susceptible to changes in sales and needs a higher amount of sales to cover its costs. Some examples of such companies the Active Growth Fund is Aiming to avoid is the retirement sector in New Zealand and banks in Australia.

The top 10 investments of the fund can be observed in the following table as of December 2019:

| Name | % of Fund net assets | Type | Country | Credit rating |

| 1. Spark New Zealand Ltd | 3.35% | Australasian Equities | New Zealand | |

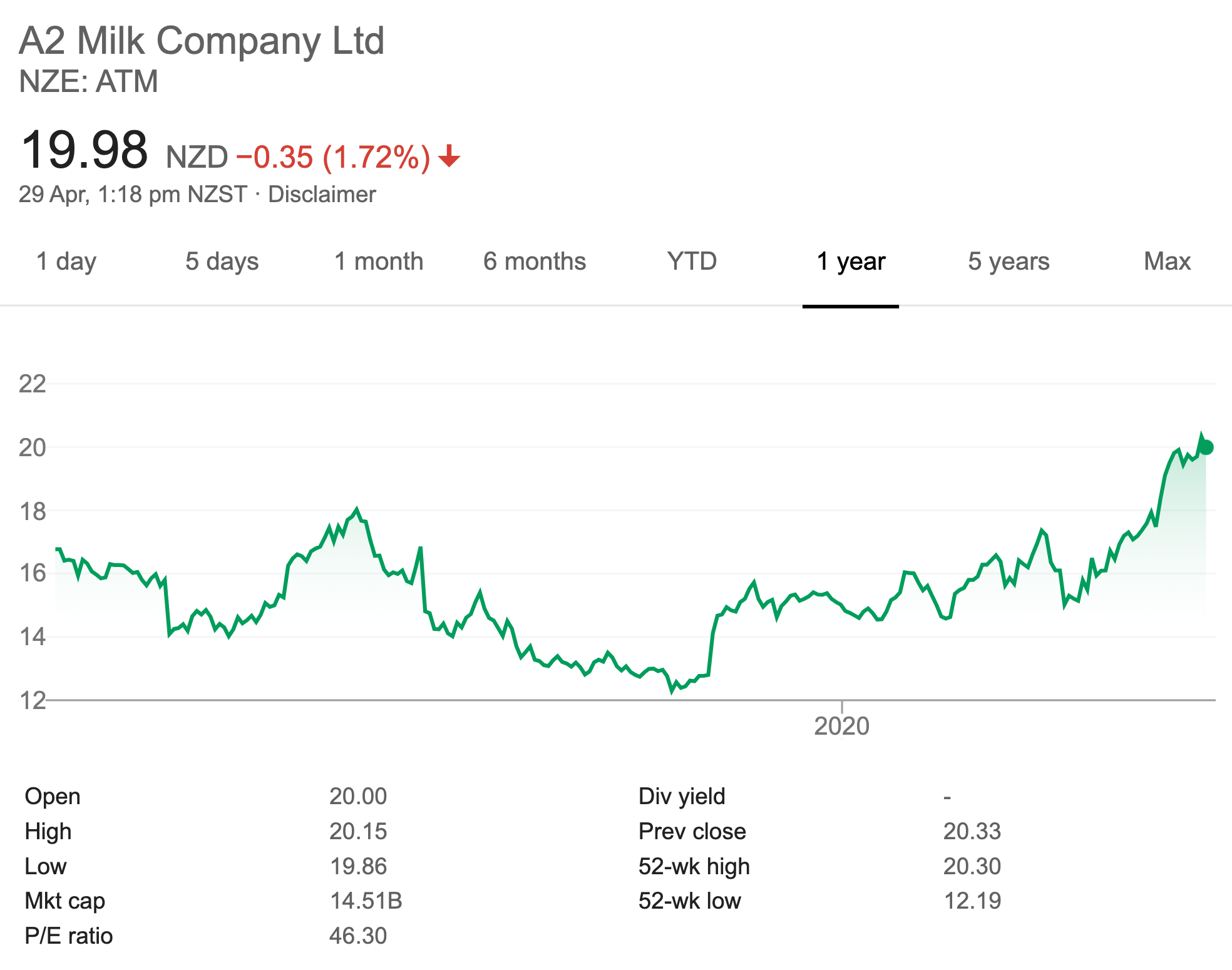

| 2. A2 Milk Company Ltd | 3.31% | Australasian Equities | New Zealand | |

| 3. Contact Energy Ltd | 3.16% | Australasian Equities | New Zealand | |

| 4. iShares MSCI EAFE Min Vol ETF | 2.63% | International Equities | United States | |

| 5. NZD Cash Current Account (NAB Bank) | 2.50% | Cash and cash equivalents | New Zealand | AA- |

| 6. EBOS Group Ltd | 2.11% | Australasian Equities | New Zealand | |

| 7. Visa Inc. – Class A | 1.91% | International Equities | United States | |

| 8. Microsoft Corporation | 1.83% | International Equities | United States | |

| 9. Summerset Group Holdings Ltd | 1.71% | Australasian Equities | New Zealand | |

| 10. HCA Holdings Inc | 1.54% | International Equities | United States |

(Source: Milford Asset Management)

In terms of specific companies, where has Milford been focusing the Active Growth Fund?

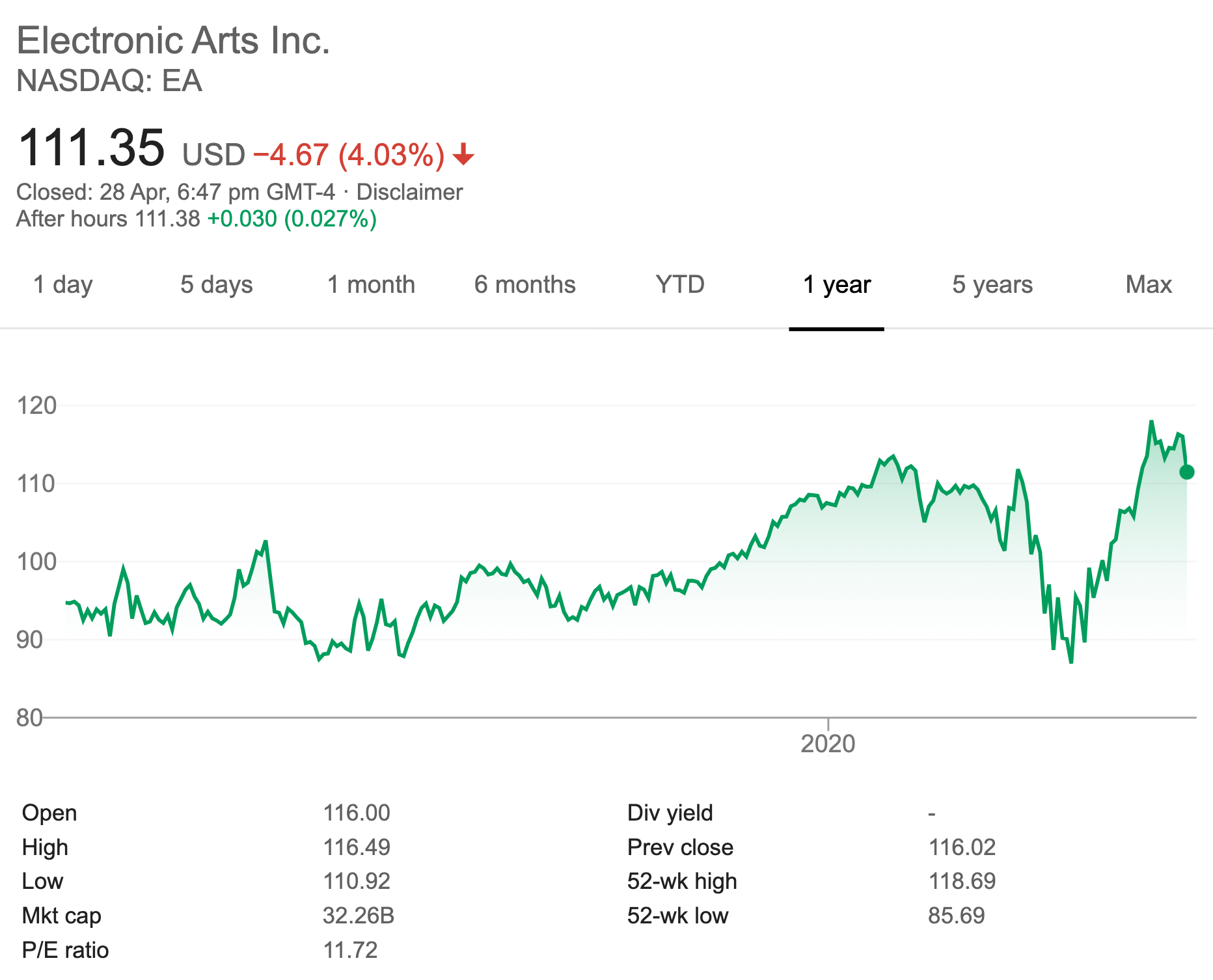

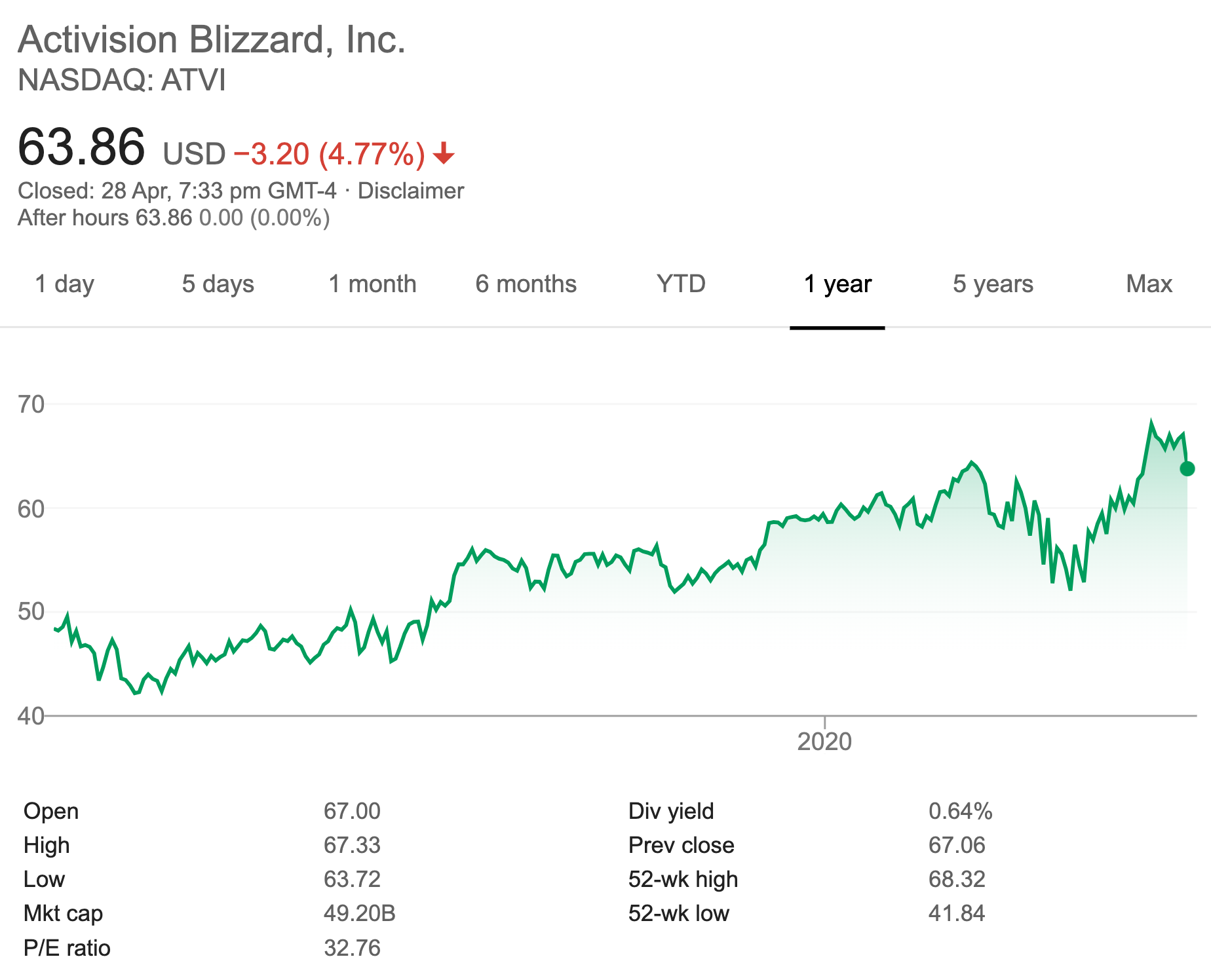

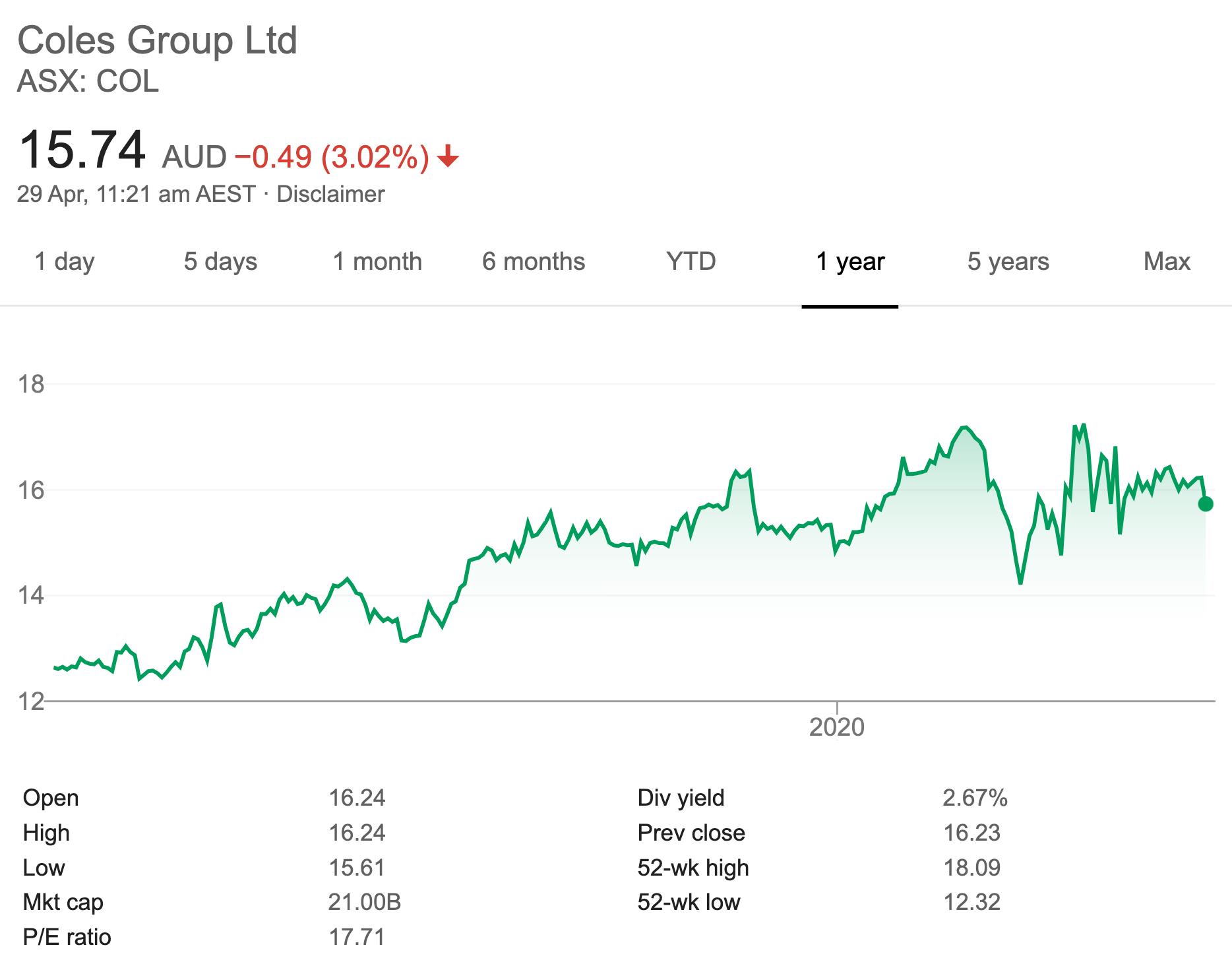

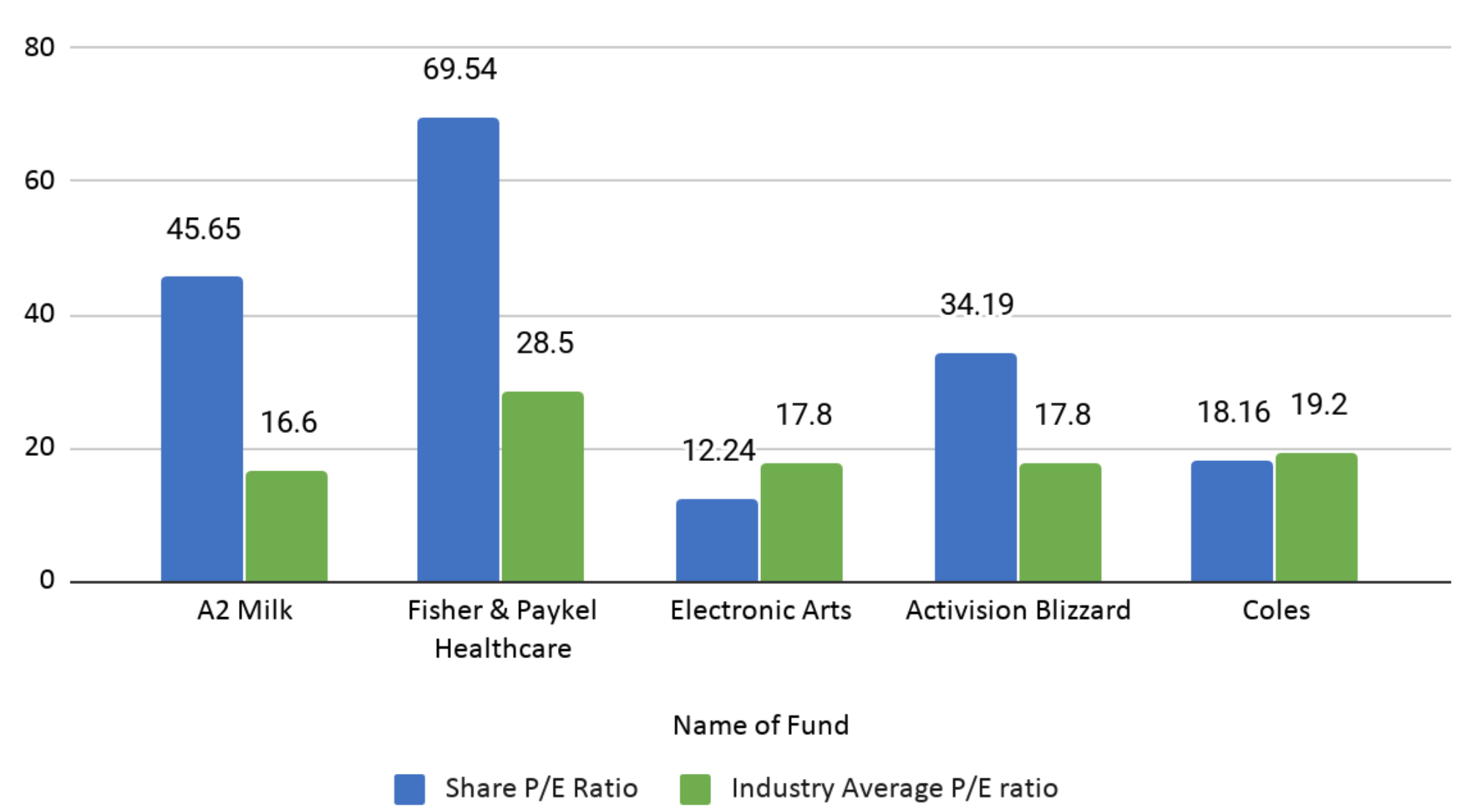

The Active Growth Fund is focussing on a few companies that are beneficiaries of the current situation caused by the coronavirus. A few examples are A2 Milk and Fisher and Paykel healthcare in NZ/Australia. In the United States, the fund has invested into video game makers Electronic Arts Sports (EA) and Activision Blizzard. Milford believes both these companies would benefit as people are locked in their homes and will be looking for cheap forms of entertainment. The share price performance of these companies for the past year can be observed below.

Furthermore, in Australia, the fund has invested in the supermarket company Coles. Due to everyone being in lock down and only supermarket stores open, Milford believes the sales of Coles will rise. Milford has come to the conclusion that the increase in sales at Coles is going to be permanent as people will continue to eat more at home.

All of these companies have made a significant gain post the initial depression in March 2020. To evaluate how the companies are performing in comparison to their competitors we analyse their price to earnings (P/E) ratio against the industry average P/E ratios. The price-to-earnings ratio or P/E is one of the most widely-used stock analysis tools used by investors and analysts for determining the stock valuation. A higher P/E ratio means that buyers have to pay a higher price for each NZ$1 the company has earned over the last year. That isn’t necessarily good or bad, but a high P/E ratio implies relatively high expectations of what a company can achieve in the future. In addition to this, it shows whether a company’s stock price is overvalued or undervalued. Observing the P/E ratio of these companies tells us what the performance expectations of these shares are.

Share P/E Ratio vs Industry Average P/E Ratio

(Source: Simplywall.st)

What are some of the opportunities being presented right now?

Milford asserts that as the world has moved through the Coronavirus crisis, markets have started to factor the effect of this into the share price of company’s. Milford has started to look at some of the companies that are oversold because of the impact of the Coronavirus. This has enabled Milford to participate in the discounted capital raising conducted by companies acting to shore up their balance sheet. A company shoring up its balance sheet indicates it is strengthening its balance sheet by raising equity capital and reducing debt.

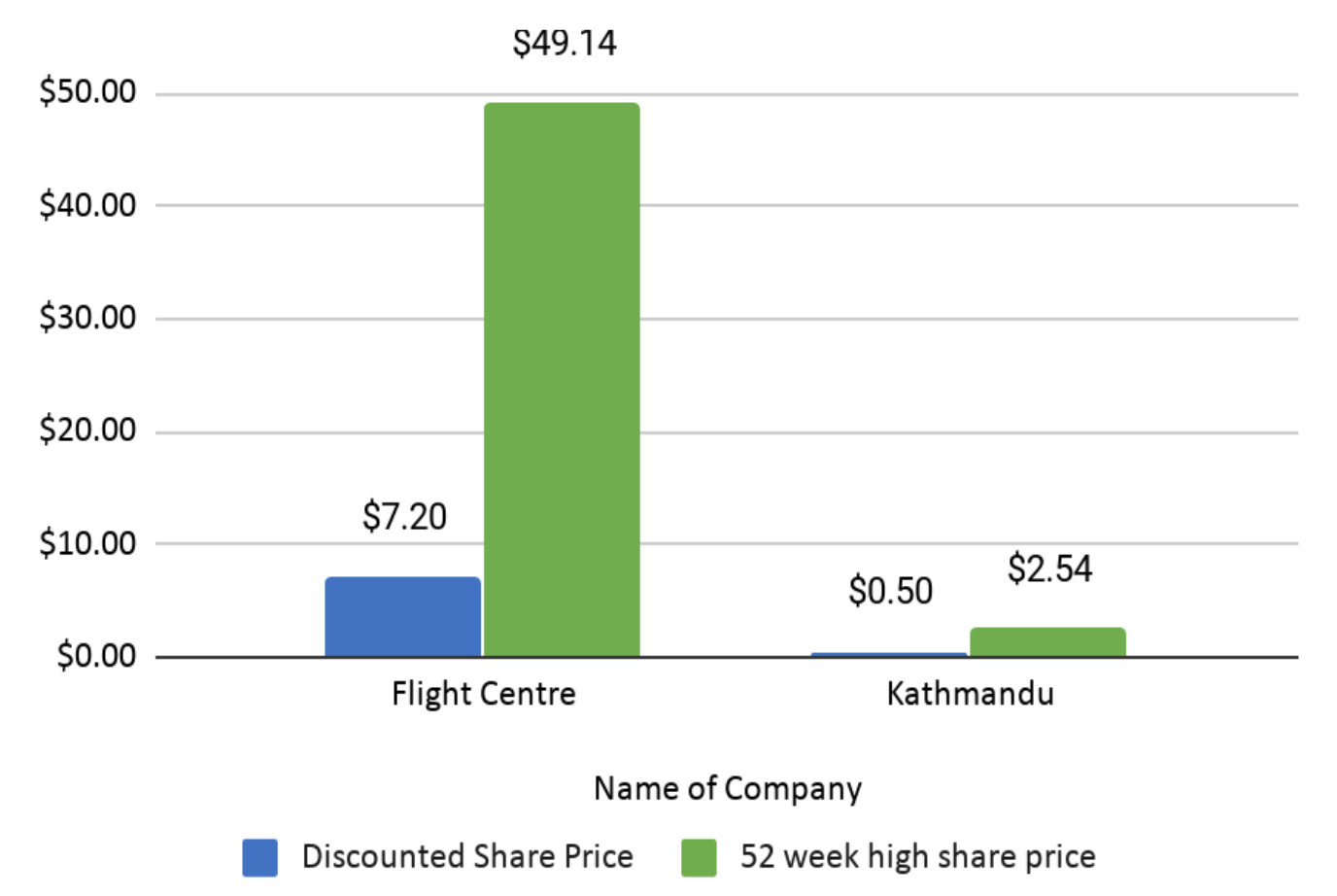

These companies that Milford mentions are Flight Centre in Australia and Kathmandu in New Zealand. Milford understands Flight Centre has been impacted by having nearly zero revenue with the travel sector closing down, while Kathmandu is a retailer experiencing no sales but continued expenses. In the first part of Milford’s analysis, they evaluated if both these companies are raising enough capital to get through an extended period of lockdown and in both case’s Milford was comfortable with their findings.

Looking at the specifics of Flight Centres and Kathmandu’s equity raising announcement we uncover the following details:

Flight Centre & Kathmandu Share Prices

Source:

Source:

- Offer Documents Kathmandu Holdings Limited (NZX/ASX: KMD)

- Operational update and equity raising

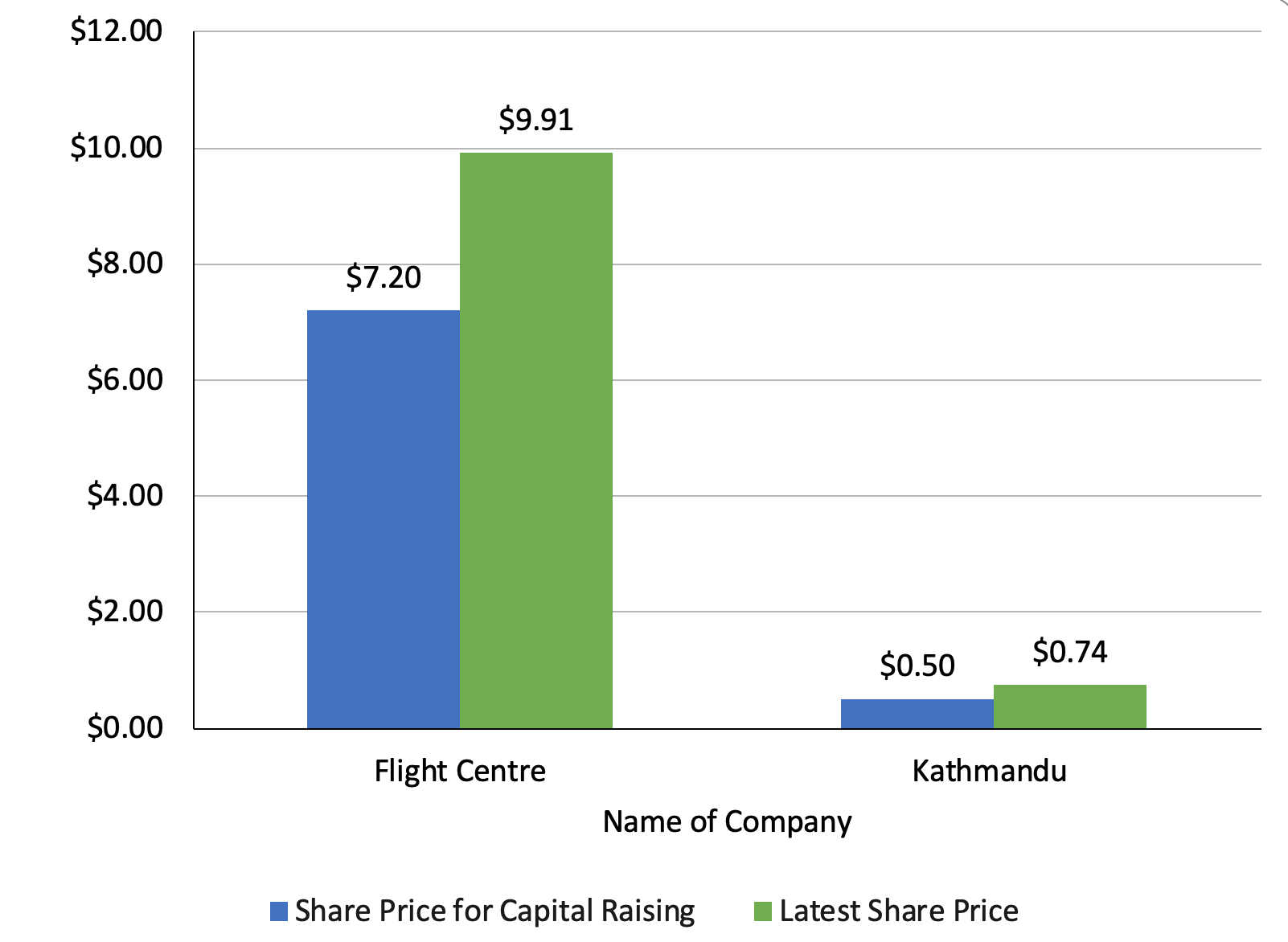

Furthermore, Milford then evaluated the post COVID-19 scenario for these businesses and formulated that earnings post COVID-19 will continue to be impaired for both these businesses by around 80%. Even with the lower levels of earning of around 80%, Milford is confident that these companies are attractively valued. In the case of Kathmandu, Milford predicts that over the next couple of years the company is projected to produce earnings five times more than what they are currently making (which is less than half of what the company’s shares typically trade at). According to Milford both Flight Centre and Kathmandu have performed well since they came out of the capital raising with a percentage change of 34.6% for Flight Centre and 48% for Kathmandu as of their latest traded share price.

Share Price at Capital Raising VS Latest Share Price

Milford state while they are focusing on such companies that are oversold like Flight Centre and Kathmandu, which in the medium-term have attractive business models, they are actively staying away from fuel beneficiaries.

Where to from here and what are the key indicators Milford is looking at?

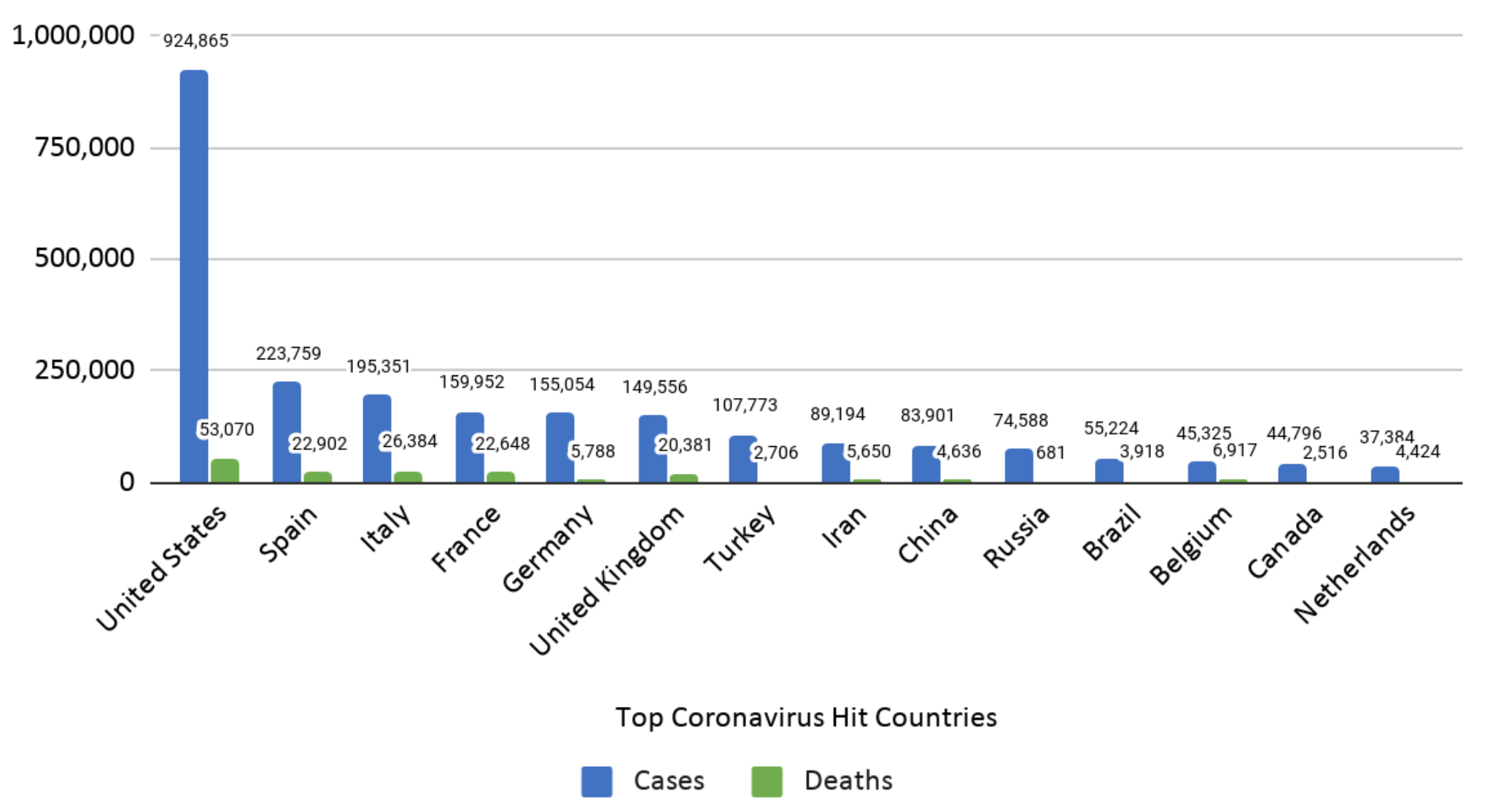

Milford is currently looking at three main areas or indicators in the market. First is the course of the virus, which continues to be highly uncertain. Milford is diligently listening to independent expert calls which state that the virus is going to be difficult to contain, especially in overseas countries where in some cases it has spread beyond the control of local governing organisations.

COVID-19 Cases & Deaths

(Source: Aljazeera) latest Updated 25th April

Second, Milford is focused on the economic impact of the virus. Milford understands this is extremely severe at the moment although they acknowledge that the central banks and governments around the world are making strong moves to help cushion the economy. Milford recognises that even with these measures by the authorities, some sectors are going to be impacted indefinitely. Therefore they are looking at time horizon estimates of how long the coronavirus will last, along with the measures taken by central banks and governments to stabilise the economy.

The third thing Milford continues to monitor is the market’s pricing for water and potential opportunities arising from these markets. The majority of Milford’s team is focusing on surveying the market, evaluating and talking to the companies. The aim of this is to figure out what their earnings are going to be in a bid to isolate attractive opportunities for the medium term.

To conclude, Milford continues to investigate attractive investment opportunities following the recent market conditions. They understand the potential benefits and drawbacks associated with various scenario differing levels of risk and scenario possibilities. The financial markets are very intricate and cannot be predicted easily. Milford understands the potential benefits and drawbacks associated with differing levels of risk and various scenarios outcomes. Using an active fund management approach will allow Milford to capitalise on opportunities revealed by major movements in the financial markets. However, Milford will proceed with caution cautious due to the degree of uncertainty in the markets.

Note: This article is based on information provided in an interview by Jonathan Windust portfolio manager and deputy CIO for Milford Active Growth Fund to Milford’s clients.